Interest spreads hold sway over the global economy

By Colin Twiggs

September 6, 2019 9:30 p.m. EDT (11:30 a.m. AEST)

First, please read the Disclaimer.

Important News

Dear Friends,

I have been writing the Trading Diary newsletter for almost 20 years. It has been a great success but times are changing. Advertisers have largely migrated to Google & social media and independent advertising through brokers has slowed to a trickle. We have therefore decided to change the format of the newsletter in line with these developments.

In future, market analysis will be provided by way of subscription through The Patient Investor. The format will remain the same, with regular updates focused on major markets — stocks, precious metals, commodities, interest rates and the economy — and increased coverage of sectors and industries.

While the change may seem sudden, the changes in advertising revenue have been evident for more than a year and I have been postponing the inevitable for some time.

Details of subscriptions are available at The Patient Investor and include a $1 subscription for the first month.

Thank you for your support.

Interest spreads hold sway over the global economy

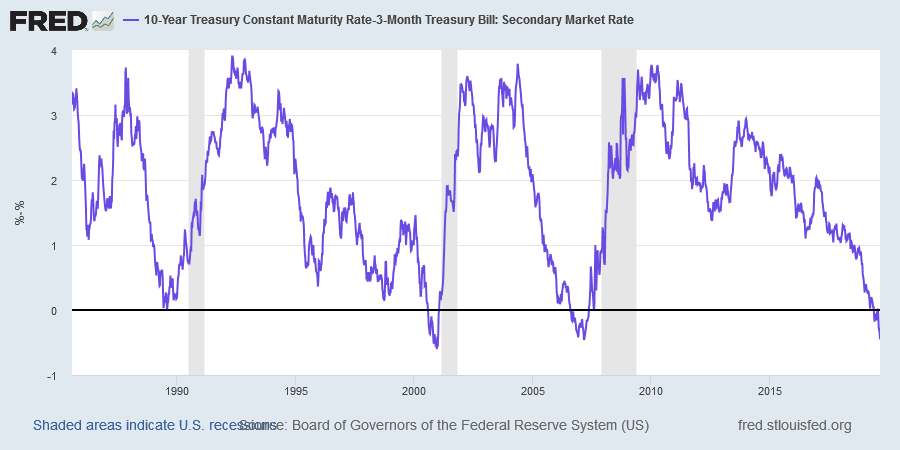

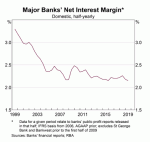

An inverted yield curve is a reliable predictor of recessions but it also warns of falling bank profits. When the spread between long-term Treasury yields and short-term rates is below zero, net interest margins are squeezed.

In a normal market, with a steep yield curve, net interest margins are wide as bank's funding maturity is a lot shorter than their loan book. In other words, they borrow short and lend long. Few bank deposits have maturities longer than 3 to 6 months, while loans and leases have much longer maturities and command higher interest rates.

When the yield curve inverts, however, the spread between long and short-term rates disappears and interest margins are squeezed. Not only is that bad for banks, it's bad for the entire economy.

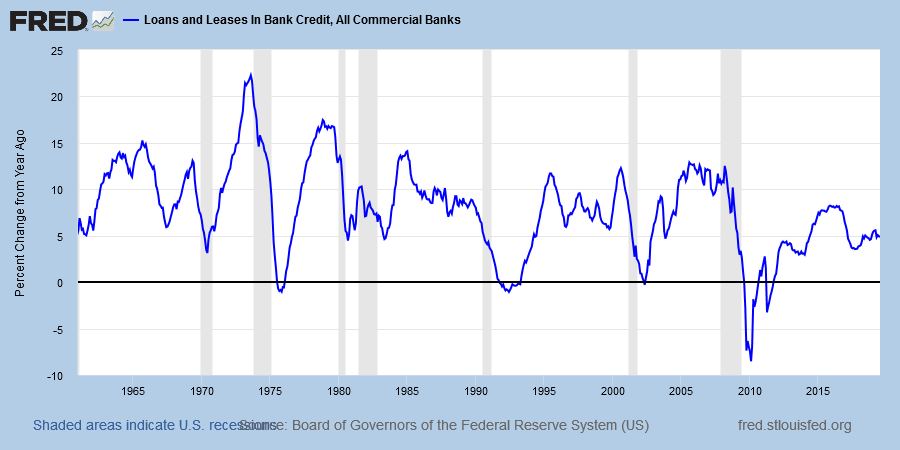

When their interest margins are squeezed, banks become risk averse and lending growth slows. That is understandable. When interest margins are barely covering operating expenses, banks cannot afford credit write-downs and become highly selective in their lending.

Slowing credit growth has a domino-effect on business investment and consumer spending on durables (mainly housing and automobiles). If there is a sharp fall in credit growth, a recession is normally not far behind1.

Right now, the Fed is under pressure to cut interest rates to support the US economy. While this would lower short-term rates and and may flatten the yield curve, cutting interest rates off a low base opens a whole new world of pain.

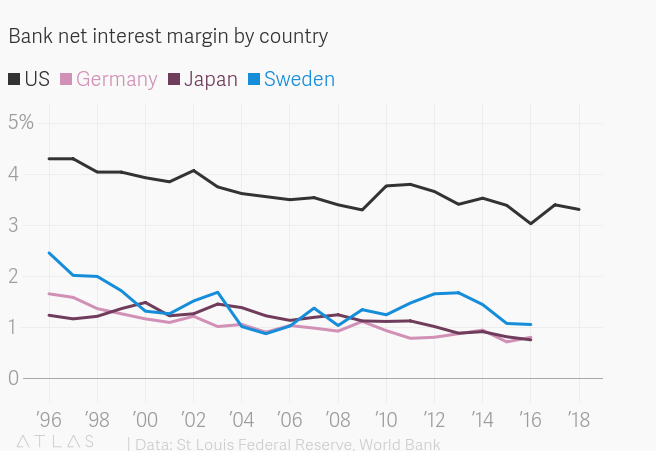

Quartz this week published a revealing commentary on the damage that negative interest rates in developed economies are doing to bank net interest margins :

The problem for commercial banks is that government bond and mortgage interest rates keep going lower, but it isn't as easy to cut deposit rates — the rate at which banks themselves borrow from customers — at the same pace. After all, it's tough to convince people to keep deposits in an account that returns less than they put in (even though this already happens, invisibly, through inflation).

Ultra-low interest rates are likely to squeeze bank margins in a similar way to the inverted yield curve. And with a similar impact on credit growth and the economy.

If I was Trump I would be pleading with the Fed not to cut interest rates.

"What beat me was not having brains enough to stick to my own game — that is, to play the market only when I was satisfied that precedents favoured my play."

~ Jesse Livermore

Footnote: 1. The NBER declared a recession in 1966 when the S&P 500 fell 22% but later changed their mind and airbrushed it out of history.

Latest

-

Global Economy

A sobering assessment [VIDEO]. -

ASX

Expect stubborn resistance. -

Australia

The elephant in the room -

S&P 500

S&P 500

Buying pressure but payrolls disappoint. -

Global economy

Global economy

Approaching stall speed. -

The long game

The long game

Why the West is losing. -

S&P 500

Buybacks are hurting growth. -

S&P 500

Rate cuts and buybacks — the emperor's new clothes. -

S&P 500

A good time to be cautious. -

PEmax

Why you should be wary of Robert Shiller's CAPE -

Portfolio

Investing in a volatile market - April 2018

Disclaimer

Colin Twiggs is director of The Patient Investor Pty Ltd, an Authorised Representative (no. 1256439) of MoneySherpa Pty Limited which holds Australian Financial Services Licence No. 451289.

Everything contained in this web site, related newsletters, training videos and training courses (collectively referred to as the "Material") has been written for the purpose of teaching analysis, trading and investment techniques. The Material neither purports to be, nor is it intended to be, advice to trade or to invest in any financial instrument, or class of financial instruments, or to use any particular methods of trading or investing.

Advice in the Material is provided for the general information of readers and viewers (collectively referred to as "Readers") and does not have regard to any particular person's investment objectives, financial situation or needs. Accordingly, no Reader should act on the basis of any information in the Material without properly considering its applicability to their financial circumstances. If not properly qualified to do this for themselves, Readers should seek professional advice.

Investing and trading involves risk of loss. Past results are not necessarily indicative of future results.

The decision to invest or trade is for the Reader alone. We expressly disclaim all and any liability to any person, with respect of anything, and of the consequences of anything, done or omitted to be done by any such person in reliance upon the whole or any part of the Material.

Please read the Financial Services Guide.